Understand The Cues From The Residential Market This Festive Season

The National Housing Board (NHB)

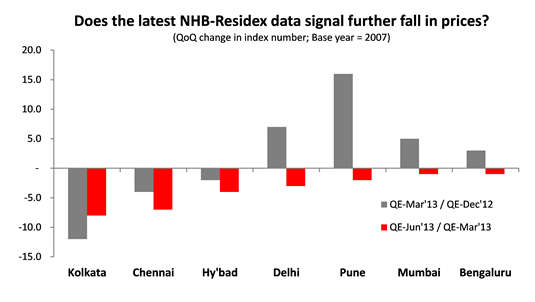

recently published its quarterly index data for the period April to June

2013. The data for the top seven cities suggest an across-the-board

fall in residential property prices in the latest quarter ending June

2013, as against a rise in price in the previous quarter (January-March

2013).

With the latest data getting wide

media attention, the question in the minds of many individuals who

intend to buy a first or second home this festive season is – are prices

beginning to correct? Should one defer purchase decisions and

potentially benefit from lower rates few months down the line?

Various channels have interpreted

this data as early signals of a broad-based price correction. The fact

is that while residential inventory seems to have indeed piled over the

last few years, prices continue to remain high in major metro cities.

This is also corroborated by the NHB Residex city indices, which

suggests that the fall in prices in the most recent quarter has been

largely a phenomenon limited to smaller cities such as Kolkata, Chennai

and Hyderabad, rather than big metros. The data certainly does not

signal an imminent price correction across the board.

Yet another belief being entertained

on various fronts is that a certain section of developers, given the

current levels of inventory and industry slackness, will be forced to

reduce prices considerably. While inventory pile-up is certainly a

reality, the real question is whether this is sufficient cause for

developers to offer considerable discounts to individual buyers.

Overall unsold inventory in cities

like Mumbai is high (as per JLL REIS data, Greater Mumbai has close to

48 months unsold inventory as against an acceptable level of 15 months).

However, a major part of this unsold inventory lies in the Island City,

which was never affordable to small individual buyers. On the other

hand, in the comparatively more affordable suburban locations, vacancy

is relatively lower and prices have not corrected as expected. They

have, in fact, remained stable or risen. Therefore, if anyone benefits

from this current scenario, it is either bulk-buying institutions or

HNIs or NRIs.

In a depressed economy where

cash-conservativeness is the watchword, it could be a natural tendency

to postpone a major financial commitment such as buying a home. Often,

individuals are tempted to time the market in an attempt to buy cheap,

on the basis of interpretations that do not reflect ground realities.

It is pertinent to note that, in a

growing economy, property always appreciates over the long term. It

never does a complete about-turn to march in the opposite direction,

though it could occasionally deviate from ‘learned’ market predictions.

Such deviations are not necessarily corrections in the commonly

understood sense of the term – they could be minor course alterations

that any market must undergo in order to adapt and stay dynamic.

Those who intend to buy residential

property during the festive season out of personal / traditional reasons

are likely tend to proceed with their purchases. For the rest, the

question would be whether one should attempt to time the market.

We believe this question is more apt

for an investor who has the potential to wait, watch and put his

financial muscle to test. Individual end users, on the other hand, will

need to establish whether the financial pain of an identified

residential project is sufficient reason for him to mark down the

pricing of units and thereby send out signals of a price correction into

the market.

That said, actual cash discounts are

definitely not out of question. Buyers with cheque books and/or

pre-approved home loans in hand are certainly in a position to bargain

for a better price. However, caution must be maintained before assuming

complete slackness of sales at the developer’s end. As already

mentioned, no developer will confirm such a state of affairs and risk

sending out distress signals to other potential customers. Demonstrable

earnestness of interest in the project, backed by ability to make a

down-payment, is the best position from where to pitch for a discount.

Also, while certain new projects in a

location may have been launched at slightly lower rates, they could be

at planned or under-construction stage. Ready-to-move-in properties in

the same location will not display the same pricing, as demand for ready

units is always the highest.

by Om Ahuja, CEO – Residential Services, Jones Lang LaSalle India

Source : Core Sector Communiqué

0 comments